What a Comparative Market Analysis is, how it works across residential and commercial real estate, and why it is the starting point for every credible pricing decision.

Before any property is listed, any offer is written, or any loan is approved, someone has to answer one fundamental question: what is this property actually worth? The answer almost always begins with a Comparative Market Analysis (CMA). Whether the decision-maker is a first-time homebuyer, a seasoned apartment investor, or a business owner evaluating a lease-versus-buy decision, the CMA anchors pricing to documented market transactions. Understanding how it works, and where it can mislead, is essential for anyone active in real estate.

What Is a Comparative Market Analysis?

A Comparative Market Analysis (CMA) is a structured evaluation of a property’s value based on recent sales of similar properties in the same market. Rather than relying on listing prices, gut feeling, or tax assessments, a CMA grounds its estimate in actual transaction data: what buyers have demonstrably been willing to pay for comparable assets. The logic is that markets are efficient over time, and recent closed sales in the same area provide the most reliable proxy for current value. A CMA formalizes that reasoning and documents the adjustments made for property-specific differences.

A CMA does not tell you what a property is worth in theory. It reflects what the market has actually paid, which is the only definition of value that matters when a transaction is imminent.

Residential vs. Commercial: Two Different Methodologies

The CMA concept applies across all property types, but the methodology diverges significantly depending on whether the analysis covers a home or an income-producing commercial asset. Both approaches start with comparable sales, but the data points, adjustments, and conclusions look substantially different.

| Comparison Point | Residential Home & Condo CMAs | Commercial Property CMAs |

|---|---|---|

| Primary basis | Driven by physical characteristics and recent buyer transactions. Comps are sourced from MLS data and must be recent, nearby, and physically similar. | Driven by income potential and investor return expectations. Comps are analyzed for cap rates, NOI, and lease terms, not physical similarity alone. |

| Primary metric | Price per sq ft | Cap rate / price per sq ft |

| Key adjustments | Beds, baths, condition | NOI, lease structure, tenancy |

| Data source | MLS / public records | CoStar, LoopNet, broker networks |

| Lookback window | 90 to 180 days typical | 12 to 24 months typical |

| Prepared by | Real estate agent / broker | Commercial broker / analyst |

| Typical cost | Free, often provided as an agent service | Free to $2,500+ depending on scope |

How a Residential CMA Is Built

A residential CMA follows a disciplined process that experienced agents complete in hours. The steps below describe how it is done properly — a useful benchmark whether the analysis is being prepared or reviewed.

| Step | Description |

|---|---|

| 1. Define the subject property | Document every physical attribute: square footage, bedroom and bathroom count, lot size, year built, garage, pool, condition, and any upgrades. This is the baseline for all comparisons. |

| 2. Select comparable sales (“comps”) | Pull recently sold properties, ideally within the past 90 days, within a half-mile radius, and within 20% of the subject’s square footage. In thin markets, these parameters may need to expand. |

| 3. Adjust for differences | No two properties are identical. Each meaningful difference between a comp and the subject receives a dollar adjustment. The comp is adjusted to reflect what it would have sold for if it were identical to the subject property. |

| 4. Analyze active listings and pending sales | Active listings define the current competition. Pending sales signal where the market is heading. Both inform the final pricing recommendation. |

| 5. Reconcile into a value range | The adjusted sale prices of the comps are reconciled into a price per square foot range and an estimated value range for the subject property. |

The Adjustment Grid

The core of any CMA is the adjustment grid: a side-by-side comparison of the subject property against each comparable sale, with dollar adjustments for every meaningful difference. The example below covers a 3-bedroom, 2-bath, 1,850-square-foot home in good condition without a pool.

| Property | Sale Price | Sq Ft | Beds / Baths | Pool | Condition | Adjusted Value |

|---|---|---|---|---|---|---|

| Subject | N/A | 1,850 | 3 / 2 | No | Good | N/A |

| Comp 1 | $435,000 | 1,920 | 3 / 2 | No | Good | $428,500 |

| Comp 2 | $418,000 | 1,780 | 3 / 2 | Yes | Average | $432,000 |

| Comp 3 | $441,000 | 1,860 | 4 / 2 | No | Good | $421,000 |

| Indicated value range | $421,000 to $432,000 | |||||

In this example, Comp 1 sold at a premium because it was larger, so the adjusted value is lower. Comp 2 had a pool and worse condition, producing upward and downward adjustments that partially offset each other. Comp 3 had an extra bedroom, adjusted down accordingly. The reconciled range, $421,000 to $432,000, gives the agent and seller a defensible pricing foundation.

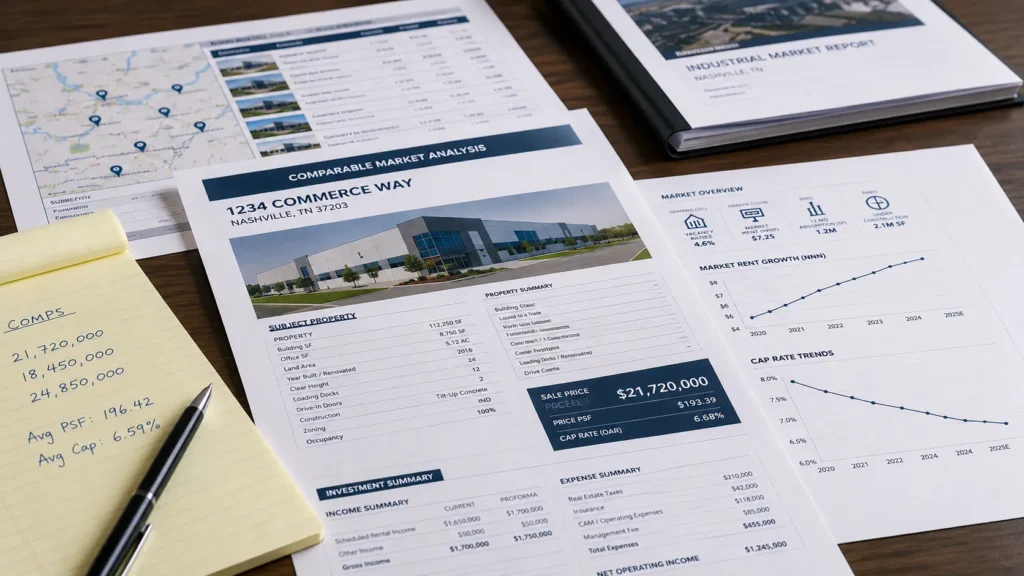

How Commercial CMA Analysis Differs

In commercial real estate, the CMA still uses comparable sales, but the analysis incorporates income and investor economics alongside physical comparisons. A standalone sale price tells only part of the story. The critical question is what the property was producing, and what return investors accepted for that income stream.

A commercial comp analysis typically captures the following:

- Sale price and price per square foot: the physical comparison baseline, consistent with residential methodology.

- Cap rate at time of sale: the yield the buyer accepted. This is often more revealing than the absolute price.

- Occupancy at time of sale: a fully leased building and a 60%-occupied building are fundamentally different assets, even at the same price per square foot.

- Lease structure and remaining term: triple-net (NNN) versus gross leases, expiration schedules, and renewal options all affect value.

- Tenant profile: national credit tenants compress cap rates; local operators expand them.

Because commercial transactions are less frequent and less publicly reported than residential sales, commercial CMAs often require access to subscription platforms such as CoStar or strong broker networks to source reliable comp data.

CMA vs. Formal Appraisal

These two terms are often conflated, even by people who have been through the real estate process. They are related but serve distinct purposes and carry different legal weight.

| Comparative Market Analysis (CMA) | Formal Appraisal |

|---|---|

| Prepared by a licensed real estate agent or broker | Conducted by a certified, state-licensed appraiser |

| Used for pricing strategy and negotiation | Required by lenders before financing is approved |

| Typically free, part of standard agent services | Costs $300 to $600+ for residential; $1,500 to $5,000+ for commercial |

| Not accepted by lenders for financing decisions | Legally binding opinion with professional liability |

| Informal opinion of current market value | Uses comparable sales, income, and cost approaches |

| Completed in hours to days | Formal written report, completed in days to weeks |

A CMA establishes the right listing or offer price. A formal appraisal is what a lender requires before committing capital. Both often arrive at similar numbers, but they differ in methodology, accountability, and downstream legal effect.

Who Uses a CMA and When

| 01 Sellers pricing a listing A CMA is the standard tool for setting an asking price. Overprice, and the property sits. Underprice, and you leave money on the table. A quality CMA threads that needle. | 02 Buyers crafting offers Buyers use CMAs to determine whether a listed price is justified — and to build the case for a lower offer or walk away from an overpriced deal. |

| 03 Investors underwriting acquisitions In commercial real estate, CMA data informs go/no-go decisions on acquisitions, refinancing, and portfolio valuations. | 04 Estate and divorce proceedings When property must be divided or valued for legal purposes, a CMA often serves as a preliminary step before a formal appraisal is ordered. |

| 05 Tax assessment appeals Property owners disputing an assessed value can use CMA data to demonstrate that the assessment exceeds actual market value. | 06 Lenders and loan officers While lenders ultimately rely on formal appraisals, CMAs provide quick preliminary guidance on whether a loan amount is in the right ballpark. |

Where CMAs Produce Unreliable Results

A CMA is only as reliable as the data behind it and the judgment applied to it. Several failure modes recur consistently across markets.

- Stale comparables. In a rapidly moving market, transactions from six months ago may no longer reflect current conditions. A rising market requires recent data; using older comps can materially underprice a listing.

- Cherry-picked data. An agent representing a seller has an incentive to select the highest comps available. An agent representing a buyer has the opposite incentive. The selection rationale should always be visible in the analysis.

- Thin market comparables. In rural areas, unusual property types, or highly customized homes, there may be very few true comparables. Stretching geographic or physical similarity parameters too far produces conclusions that are difficult to defend.

- Unquantified qualitative factors. A CMA captures what has sold. It does not always capture why. A property on a high-traffic road may have sold at a discount that a grid adjustment will not fully reflect.

- List price substituted for sale price. A CMA based on active listings reflects seller expectations, not market reality. Only closed transactions establish what buyers actually paid.

A credible CMA documents every adjustment and explains why each comparable was included. If the reasoning is not visible in the analysis, the analysis is incomplete.

Why This Tool Matters Across Real Estate Disciplines

CMAs connect directly to the broader analytical framework of real estate finance. In commercial real estate, cap rates are derived from comparable transactions: the market’s accepted yield for a given property type and location is itself a product of CMA-style analysis. In residential real estate, the CMA is the bridge between a seller’s expectations and what a buyer will pay.

For buyers, understanding how a CMA is built means the agent’s pricing recommendation can be evaluated on its merits rather than accepted on faith. For sellers, it provides the basis to defend a strong asking price or push back on a lowball listing suggestion. For investors, it supplies the vocabulary to interrogate a broker’s underwriting assumptions at the source.

In any market, rising or falling, residential or commercial, a CMA is where defensible pricing decisions begin.

How BlueStar Consulting Approaches Market Analysis

BlueStar Consulting provides market analysis and underwriting support to investors and developers evaluating commercial acquisitions, portfolio repositioning, and development feasibility. Our market analysis engagements go beyond comparable sales to incorporate cap rate trends, submarket absorption data, and supply pipeline projections relevant to the specific asset and investment thesis. Investors working through an acquisition or a portfolio valuation can engage BlueStar for a structured market and financial analysis tailored to their deal parameters.

Comparative Market Analysis in Real Estate Frequently Asked Questions

What is the difference between a CMA and an appraisal?

A CMA is an informal opinion of market value prepared by a licensed real estate agent or broker, typically as part of the listing or buyer representation process. It is used for pricing and negotiation decisions but is not accepted by lenders. A formal appraisal is conducted by a certified, state-licensed appraiser, carries professional liability, and is required by lenders before financing is approved. Both use a comparable sales approach, but an appraisal additionally incorporates income and cost approaches for commercial assets.

How far back should comparable sales go in a CMA?

For residential properties in active markets, 90 days is the standard lookback window. In slower markets or for unusual property types, 180 days is common. Commercial CMAs typically look back 12 to 24 months because transaction volume is lower and individual sales carry more weight. In either case, the analyst should note whether market conditions have shifted materially during the lookback period, as older transactions may require directional adjustments.

Can a CMA be used for commercial properties?

Yes, and in commercial real estate it is a standard component of acquisition underwriting. The methodology expands beyond physical comparisons to include cap rate analysis, occupancy at time of sale, lease structure, and tenant credit quality. Commercial CMAs typically require access to proprietary data platforms such as CoStar or Real Capital Analytics, and they are usually prepared by commercial brokers or analysts rather than residential agents.

What makes a CMA inaccurate?

The most common sources of error are stale comparables, selectively chosen comps, and insufficient adjustment discipline. In thin markets with few true comparables, geographic or physical similarity parameters are sometimes stretched further than the data can support. CMAs based on active listings rather than closed transactions are inherently unreliable because they reflect seller expectations, not actual buyer behavior. Reviewing the adjustment rationale and comp selection criteria is the most direct way to assess the quality of any CMA.

How is a CMA different from a broker opinion of value (BOV)?

A broker opinion of value, or BOV, is a more formal version of a commercial CMA, typically presented as a structured document with detailed comparable analysis, income projections, and market context. A CMA is more commonly used in residential contexts and represents a lighter analytical framework. Both are informal, non-binding estimates of market value prepared by licensed brokers rather than certified appraisers. The BOV is the standard preliminary valuation tool in commercial brokerage, particularly for larger or more complex assets.