Before a dollar of sale proceeds reaches the GP’s promote, it has to clear a queue. Return of capital first. Then a preferred return. Then a catch-up. That queue is the real estate waterfall model. How a sponsor structures it determines who benefits when a deal performs well, and who bears the cost when it does not. Whether structuring a deal or reviewing one, the waterfall is where the economic relationship between GP and LP is actually defined.

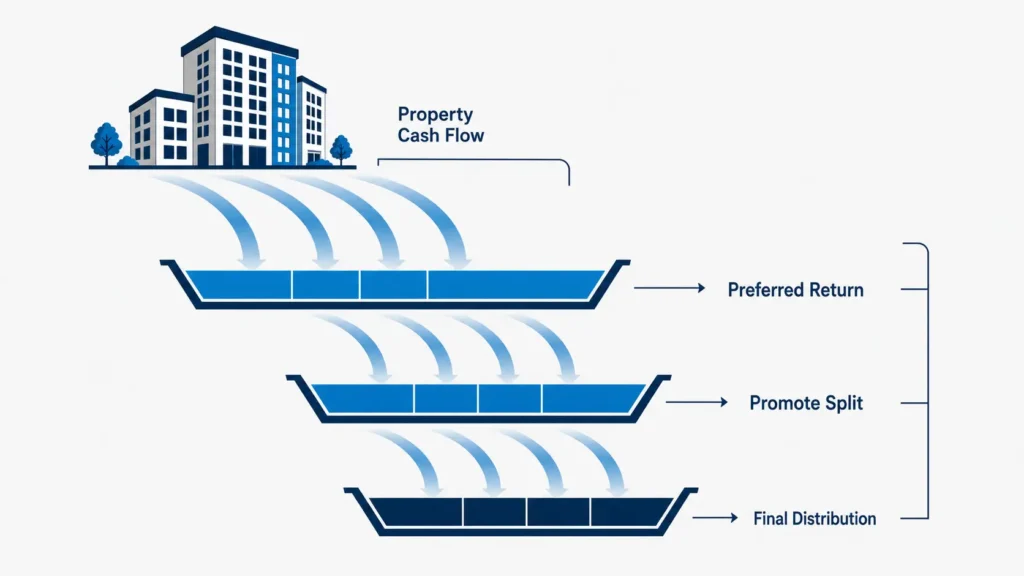

A real estate waterfall model is a tier-based framework that determines how cash flow from a property or fund is distributed between the general partner (GP) and limited partners (LPs). It runs in a fixed order: return of capital, then a preferred return to LPs, then a GP catch-up, then a carried interest split.

Each tier must be cleared before proceeds flow to the next. Pref accrual basis, catch-up percentage, hurdle structure, and deal-by-deal versus whole-fund treatment are the variables that make one waterfall differ from another.

What Is a Real Estate Waterfall?

A real estate waterfall is a contractual distribution structure. It is written into the limited partnership agreement (LPA) or operating agreement (OA) governing a deal or fund. It specifies, in exact order, how every dollar of distributable cash splits between the GP and the LP.

Why the Waterfall Structure Exists

The waterfall exists to align incentives. LPs contribute most of the equity. GPs contribute expertise, time, and often a small co-investment. Without a structure, a GP could earn a large fee regardless of performance. The waterfall gives LPs priority on capital recovery and a baseline return first. The GP’s promote, its outsized share of profit above the LP’s return threshold, is earned only when the deal outperforms.

Waterfall vs. Pro Rata Distribution

A pro rata distribution splits every dollar by ownership percentage from the first dollar. A GP owning 10% of a deal receives 10% of every distribution, regardless of performance. A real estate waterfall model replaces that flat split with tiers. LPs receive priority in early tiers. The GP’s share increases only in later tiers, after LPs clear their preferred return.

The Four Tiers of a Standard CRE Waterfall

A standard commercial real estate (CRE) waterfall runs through four tiers in sequence. Cash fills each tier completely before spilling into the next.

Tier 1: Return of Capital

Tier 1 returns 100% of contributed capital to both partners, pro rata to equity share. No pref accrues. No promote is paid. This tier sets a clean baseline: neither partner has earned a profit until the original investment is fully returned.

Tier 2: Preferred Return

Tier 2 pays LPs a preferred return, or “pref,” on contributed capital. The pref is a minimum return threshold, typically an annual percentage. This tier holds the model’s most consequential decision: does the pref accrue as simple interest, or compound like an internal rate of return (IRR)? That choice changes the dollar amount owed to LPs.

Tier 3: GP Catch-Up

Tier 3 is the GP catch-up. Once LPs receive their full pref, the GP receives a disproportionate share of cash until cumulative distributions equal its target promote percentage. A 100% catch-up means the GP takes every dollar until it reaches that target. A 50% catch-up splits the tier evenly, keeping LPs in cash flow longer.

Tier 4: Carried Interest Split (The Promote)

Tier 4 is the residual tier. All remaining cash splits by the agreed promote ratio, commonly 70/30 or 80/20 in favor of the LP. This tier has no ceiling.

Simple Interest Waterfall vs. IRR Waterfall: The Distinction Most Guides Skip

The Tier 2 pref can accrue two different ways: simple interest or IRR-based compounding. Most tutorials assume IRR without stating it. Many operating agreements specify simple interest instead. This mismatch is a common source of practitioner confusion.

How Unpaid Pref Accrues in Each Method

Under simple interest, unpaid pref accrues linearly on the original capital balance only. An 8% simple pref on $1,000,000 accrues $80,000 per year, regardless of prior unpaid amounts. Under IRR-based compounding, unpaid pref compounds on the growing balance, including previously unpaid pref. The same 8% IRR pref grows faster each year a distribution is skipped.

The Economic Difference on a Deal That Underperforms

The gap between the two methods widens as a hold period lengthens. An IRR-based pref can owe LPs a materially larger balance than simple interest on the same capital and rate. A deal that underperforms and delays distributions makes this gap larger, not smaller.

Which Method Is More Common in Operating Agreements

Both methods appear regularly. Simple interest pref is common in single-asset syndications. IRR-based, compounding pref is standard in institutional fund structures. Confirm which method the OA specifies before building a model. The two methods produce materially different LP distributions on an identical deal.

Types of Real Estate Waterfall Structures

Waterfalls also differ by structural type. The type determines when the GP can earn carry and how much downside protection LPs retain.

Single-Tier Waterfall

A single-tier waterfall has one hurdle: return of capital plus a pref, then a flat promote split above it. It is the simplest structure, common on smaller single-asset deals.

Multi-Tier Waterfall

A multi-tier waterfall stacks multiple hurdles, each with its own IRR or equity multiple threshold and promote percentage. A common structure: pref only up to 8% IRR, an 80/20 split from 8% to 12%, and a steeper 70/30 split above 12%. Multi-tier structures reward GPs more as performance improves.

American (Deal-by-Deal) Waterfall

An American waterfall calculates promote on each individual deal, not the fund as a whole. GPs get paid carry earlier. It also creates clawback risk: if early deals perform well and later deals underperform, the GP may have been overpaid on a whole-fund basis.

European (Whole-Fund) Waterfall

A European waterfall requires all fund capital returned, plus fund-wide pref, before the GP earns any carry. This structure has minimal clawback risk by construction. Institutional LPs generally prefer it.

Hybrid Waterfall

A hybrid waterfall releases GP carry deal-by-deal, but only after a threshold percentage of fund capital, often 75%, has returned to LPs. It blends GP cash flow benefits with LP downside protection.

| Structure | Who It Favors | Clawback Risk | When Used |

| Single-tier | Neutral | Low | Single-asset deals, simple syndications |

| Multi-tier | GP, at higher performance | Moderate | Value-add and opportunistic deals |

| American (deal-by-deal) | GP | High | GP-favorable funds, faster carry realization |

| European (whole-fund) | LP | Low | Institutional funds, large LP mandates |

| Hybrid | Balanced | Moderate | Funds negotiating GP and LP priorities |

Step-by-Step Worked Example: A 3-Tier IRR Waterfall

This example models a real estate waterfall model on a five-year hold. GP contributes 10% of equity, LP contributes 90%. Total equity: $10,000,000, split $1,000,000 GP and $9,000,000 LP. Three tiers: pref only up to 8% IRR, an 80/20 split from 8% to 12% IRR, and a 70/30 split above 12% IRR.

| Year | Cash Flow |

| Year 0 | ($10,000,000) |

| Year 1 | $600,000 |

| Year 2 | $650,000 |

| Year 3 | $700,000 |

| Year 4 | $750,000 |

| Year 5 (operating + sale) | $13,200,000 |

Total distributable cash: $15,900,000.

Tier 1: Return of Capital. LPs receive $9,000,000. GP receives $1,000,000. Remaining: $5,900,000.

Tier 2: Preferred Return (8% IRR). The 8% IRR pref on the LP’s $9,000,000, compounded across five years, totals approximately $4,229,000. LP receives this in full. Remaining: $1,671,000.

Tier 3: GP Catch-Up (100%). The catch-up brings the GP to 20% of total profit distributed. Total profit through Tier 2 is $4,229,000, all to LP. The GP needs $1,057,250 to reach 20%. The tier has $1,671,000 available, so the GP receives the full catch-up. Remaining: $613,750.

Tier 4: Residual Split (70/30). The remaining $613,750 splits 70% to LP ($429,625) and 30% to GP ($184,125). Remaining after this tier: $0.

Balance check: LP total: $9,000,000 + $4,229,000 + $429,625 = $13,658,625. GP total: $1,000,000 + $1,057,250 + $184,125 = $2,241,375. Combined: $15,900,000, matching total distributable cash exactly. LP net IRR on this structure is approximately 12.1%. GP net IRR, boosted by promote on a smaller equity base, runs significantly higher, a pattern typical of a well-performing waterfall.

Clawback Provisions: LP Protection in an American Waterfall

A clawback provision protects LPs when a deal-by-deal waterfall overpays the GP relative to whole-fund performance.

What Triggers a Clawback

A clawback triggers when the GP’s cumulative carry, calculated across all realized deals, exceeds what it would earn under a final, whole-fund calculation. This happens when early deals perform well and later deals underperform. The GP received carry on early wins before knowing later losses would offset them.

How Clawback Escrows Work

The Institutional Limited Partners Association (ILPA) recommends GPs escrow at least 25% to 30% of carry distributions throughout the fund’s life, per its Private Equity Principles. Escrowed carry is not released to individual partners until a clawback test confirms no excess was paid. ILPA also recommends interim testing during the fund’s life, not only at wind-down.

Proskauer’s Private Equity Annual Review found 68% of institutional funds formed since 2020 include interim clawback testing, up from 41% in funds formed between 2010 and 2015.

Deal-Level IRR vs. LP Net IRR: Why the Difference Matters

Deal-level IRR measures return on total project cash flows before any promote is paid. It reflects the property’s performance, independent of the waterfall. LP net IRR measures what the LP actually receives after the promote is deducted. These two numbers are routinely confused. The gap between them is the actual cost of the waterfall structure to the LP.

In the worked example above, LP net IRR of approximately 12.1% sits below what a naive read of the deal’s headline return might suggest. The promote structure redirected a meaningful share of profit to the GP once performance cleared the hurdles. An LP evaluating an offering memorandum should always request LP net IRR specifically, not the deal-level or project-level IRR in marketing materials.

Market-Standard Waterfall Terms in 2025-2026

Institutional waterfall terms have shifted since 2021. Capital scarcity relative to deal flow has given LPs renewed negotiating leverage.

Preferred Return Range: 7% to 9%

Institutional preferred returns are drifting from the traditional 8% toward 9% in newer agreements. The “8 and 20” default is no longer automatically assumed.

GP Co-Invest: 1% to 5%

GP equity co-investment of 1% to 5% of total capital is standard for institutional real estate funds. It demonstrates alignment without requiring a large equity check.

Promote Percentage: 15% to 25% Above the First Hurdle

GP promote percentages of 15% to 25% above the first IRR hurdle are standard. Terms above this range are treated as a negotiation point, not a default.

Catch-Up Percentage: 100% Standard, 50% to 90% Increasingly Negotiated

A 100% GP catch-up remains the drafted market standard in many agreements. Institutional LPs increasingly negotiate this down to 50% to 90%, which slows the GP’s path to full promote and keeps LPs in cash flow longer.

Clawback Escrow: 25% to 30% of Carry, ILPA Guidance

ILPA’s 25% to 30% escrow guidance is the reference point institutional LPs cite in negotiation. Actual practice varies. Some funds escrow nothing. Some escrow 100% of interim carry.

Common Waterfall Modeling Mistakes

Four mistakes recur across sponsor-built and analyst-built waterfall models.

Measuring Hurdles at the Wrong Level

Hurdles must be measured on LP cash flows, not total project cash flows. A model triggering Tier 3 based on deal-level IRR rather than LP-level IRR misallocates the catch-up tier. The result does not match the operating agreement.

Miscalculating the Catch-Up Tier

The catch-up tier is a share of total profit distributed to date, not a share of cash available in that tier alone. A model treating Tier 3 as a simple split of its own tier’s cash produces an incorrect catch-up amount. The correct approach solves for the GP’s target cumulative share instead.

Using IRR When the OA Specifies Simple Interest Pref

This is the most common source of model-to-document mismatch in current practitioner discussion. A model built on the default IRR assumption, applied to a deal whose OA specifies simple interest pref, overstates the pref owed to LPs. It also understates what flows to GP promote tiers.

Residual Cash Remaining After the Final Tier

A correctly built model resolves to zero remaining cash after the final tier. A real estate waterfall model that leaves a residual balance has a broken tier formula, most often in the return-of-capital or catch-up calculation. The balance check in the worked example above is the standard verification step before a model is used for LP reporting.

Free Waterfall Calculator

A real estate waterfall model requires precise tier-by-tier cash flow tracking, exactly the kind of calculation prone to the errors covered above. BlueStar’s free waterfall distribution calculator handles both simple interest and IRR-based pref. It supports up to five tiers. Output includes a full year-by-year LP and GP distribution breakdown with a balance check built in. Use the free waterfall distribution calculator to run these numbers on a specific deal.

How BlueStar Consulting Approaches Waterfall Modeling

BlueStar Consulting builds and audits real estate waterfall models as part of its financial modeling and underwriting work. Each model is reconciled against the exact language of the operating agreement, not a generic template. Getting the pref accrual method, catch-up mechanics, and clawback terms right before capital moves matters. It is the difference between a model that matches the legal document and one that does not. Developers and investors working through a syndication or fund structure can engage BlueStar for a waterfall model build or a second-opinion review.

Frequently Asked Questions

What is a real estate waterfall model?

A real estate waterfall model is a tier-based structure defined in the limited partnership agreement. It determines how cash flow from a property or fund is distributed between the general partner (GP) and limited partners (LPs). It runs in a fixed order: return of capital, preferred return, GP catch-up, and a carried interest split. Each tier must be fully paid before proceeds move to the next. The structure aligns GP incentives with LP returns by ensuring LPs receive priority before the GP earns a performance-based promote.

What is a preferred return in a waterfall?

A preferred return, or “pref,” is the minimum annual return LPs must receive on contributed capital before the GP earns any promote above its pro-rata share. It is typically 7% to 9% in current institutional deals. The pref can accrue on a simple interest basis or compound like an IRR, and the two methods produce materially different dollar amounts over a multi-year hold. Check which method a specific operating agreement specifies before building or evaluating a waterfall model.

What is the GP promote, or carried interest?

The GP promote, also called carried interest or “carry,” is the general partner’s disproportionate share of profit above the LP’s return threshold. It is the GP’s primary incentive for outperforming underwriting. A GP owning 10% of a deal’s equity might earn 20% or more of profit once the deal clears its preferred return hurdle. The promote is earned only in later waterfall tiers, after LPs receive capital and pref in full.

What is a catch-up provision in a real estate waterfall?

A catch-up provision is the waterfall tier where the GP receives a disproportionate share of cash, often 100%, until its cumulative distributions equal its target promote percentage. It occurs after LPs receive their full preferred return and before the final residual split tier. A 100% catch-up gets the GP to its target share quickly. A partial catch-up, in the 50% to 90% range increasingly seen in institutional deals, slows that process.

What is a clawback in a waterfall structure?

A clawback requires the GP to return excess carry if cumulative distributions, calculated deal-by-deal, exceed what it would have earned under a final whole-fund calculation. Clawbacks primarily apply to American, deal-by-deal waterfalls, since European structures have minimal clawback risk by design. ILPA recommends GPs escrow at least 25% to 30% of carry distributions specifically to fund any clawback obligation without requiring individual partners to return personal funds years later.

What is the difference between deal-level IRR and LP net IRR?

Deal-level IRR measures return on total project cash flows before any promote is deducted, reflecting the property’s underlying performance. LP net IRR measures what the LP actually receives after the GP’s promote is paid through the waterfall tiers. These numbers are commonly confused in offering materials that lead with deal-level IRR without clarifying that LP net IRR will be lower. LPs evaluating a deal should always request LP net IRR specifically.

What are market-standard waterfall terms for CRE deals in 2025?

Current institutional norms: preferred return of 7% to 9%, drifting toward the higher end in newer agreements. GP co-investment runs 1% to 5% of total equity. GP promote sits at 15% to 25% above the first hurdle. Catch-up percentage is still drafted at 100% in many agreements but is increasingly negotiated to 50% to 90%. Clawback escrow runs 25% to 30% of carry, per ILPA guidance. Terms outside these ranges are not automatically unreasonable, but they depart from current market norms and warrant closer review.