- Home

- Calculators

- Pto Forma Calculator

Commercial Real Estate

Pro Forma Calculator

Build a full pro forma in minutes: income, expenses, debt service, and exit assumptions in one model. Stress-test the line items before you commit capital, not after.

Real Estate Pro Forma Calculator

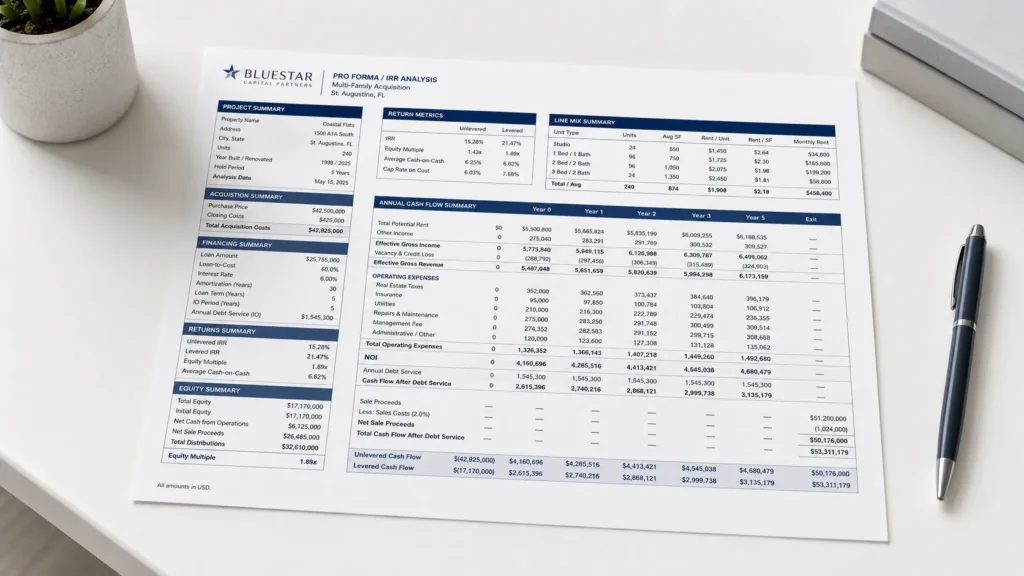

A real estate pro forma is a financial projection that estimates a property’s income, operating expenses, and investment returns over a defined hold period. It models gross potential rent, vacancy, operating expenses, net operating income (NOI), debt service, and cash flow to calculate the return metrics that drive an acquisition decision: going-in cap rate, IRR, cash-on-cash return, and equity multiple.

The calculator below builds a complete pro forma from four inputs: the purchase price and income, the operating expense structure, the growth and exit assumptions, and, if the deal is debt-funded, the financing terms. It returns a full Year 1 pro forma table built line by line, a year-by-year cash flow projection, and the six metrics a lender or investment committee will ask for first.

Who this is built for: real estate investors and developers underwriting an acquisition, analysts running a first-pass screen, or anyone reviewing a sponsor’s projections before capital changes hands.

Commercial Real Estate Pro Forma Calculator

Build a Year 1 pro forma and project IRR, NPV, equity multiple, and DSCR across the hold period. Toggle the Financing tab to compare levered and unlevered returns.

How to Use This Calculator

The calculator runs in two tabs and follows the structure of an institutional pro forma. Start in the Pro Forma tab, then toggle Financing if the deal is debt-funded.

Step 1: Enter property and income

The first card sets the deal size and top-line revenue.

- Purchase Price: total acquisition cost in dollars.

- Gross Annual Rental Income: stabilized Year 1 gross potential rent, before vacancy. For multifamily, multiply units by monthly rent by 12.

- Vacancy: slider, expressed as a percent of gross potential rent.

- Ancillary Income: percent of net rental income. Captures parking, laundry, fees, pet rent.

Step 2: Enter operating expenses

Each expense has paired percent and dollar fields. Edit either, the other updates automatically.

- Property Taxes, Insurance, Maintenance, Capital Reserves: percent calculated against purchase price.

- Management Fee: percent calculated against effective gross income (EGI), not price.

Step 3: Set growth, hold, and exit

The third card defines the projection and the exit assumption.

- NOI Growth Rate: applied to NOI each year of the hold and to the perpetuity step-up at sale.

- Hold Period: years held before sale.

- Required Return: discount rate for NPV and the hurdle the IRR is compared against.

- Exit Cap Rate: capitalization rate at which the property is sold. A higher exit cap means a lower sale price.

Step 4 (optional): Add financing

Open the Financing tab and flip the switch to enable.

- Loan Type: Amortizing for standard P&I, Interest-Only for interest payments with full principal due at sale.

- Down Payment: equity contribution. Loan amount equals purchase price minus down payment.

- Mortgage Rate: annual interest rate. Amortizing loans use a 30-year schedule.

- Minimum DSCR: lender threshold. The Year 1 DSCR result will flag pass or fail against this value.

The calculator updates with every input change. There is no submit button.

How to Read the Results

The Year 1 Pro Forma table is the foundation. The metrics grid and the year-by-year table sit on top of it.

Year 1 Pro Forma

- Walks from gross potential rental income to NOI after reserves, line by line, matching how an institutional pro forma is built.

- Total operating expenses show the OpEx ratio (percent of EGI) as a sanity check. Stabilized multifamily typically runs 35 to 45 percent.

- NOI after reserves is the number that drives the DCF, not gross NOI.

Key metrics

- Going-in Cap Rate: NOI after reserves divided by purchase price. Calculated automatically.

- Unlevered IRR: project-level return on the unlevered cash flows. The metric to use when comparing deals against each other.

- Levered IRR: return on equity after debt. The metric the equity investor cares about. Only shown when financing is enabled.

- NPV: net present value at the required return hurdle. Positive means the deal beats the hurdle, negative means it does not.

- Equity Multiple: total cash returned divided by equity invested. Ignores timing.

- Year 1 DSCR: NOI after reserves divided by annual debt service. The pill shows whether it clears the minimum DSCR threshold.

Year-by-year cash flow table

- NOI: the property’s annual operating result.

- Debt Service: annual loan payment, shown only when financing is enabled.

- Net Cash Flow: NOI minus debt service (when levered), plus net sale proceeds in the exit year.

- Cumulative: running total of cash flows from Year 0. Where this crosses zero is the payback point.

Cumulative cash flow chart

Visualizes the recovery curve. Red bars show capital still at risk. Blue bars show capital recovered and gain accumulating. The transition from red to blue is the payback year.

A strong deal pencils on every line: NOI growing, DSCR clearing the minimum with margin, IRR above the hurdle, NPV positive, equity multiple above 1.5x for a five-to-ten-year hold. A marginal deal fails on one or two. A weak deal fails on most.

What Line Items a Real Estate Pro Forma Must Include

A pro forma that omits a line item does not eliminate that cost. It just hides it until the cost shows up in an actual operating statement, at which point it compresses NOI the model never accounted for. The table below maps the line items every complete pro forma must carry, and where each one lives in the calculator above.

| Section | Line Item | What It Captures |

|---|---|---|

| Income | Gross Potential Rent | Full occupancy revenue at market rates, before any deductions |

| Income | Vacancy Loss | Revenue lost to unoccupied units, expressed as a percent of GPR |

| Income | Ancillary Income | Parking, laundry, pet rent, application and late fees |

| Income | Effective Gross Income (EGI) | Total collectible revenue after vacancy, before expenses |

| Expenses | Property Taxes | Often the single largest controllable line; reassessment risk on sale is the most common underwriting miss |

| Expenses | Insurance | Property and liability coverage, increasingly volatile in coastal and catastrophe-exposed markets |

| Expenses | Maintenance and Repairs | Recurring operational upkeep, distinct from capital reserves |

| Expenses | Management Fee | Calculated against EGI, not purchase price, since it scales with collected revenue |

| Expenses | Capital Reserves | Forward-funded replacement reserve for roofs, HVAC, and major systems |

| Below the line | Net Operating Income (NOI) | EGI minus total operating expenses; the number used for valuation and lender underwriting |

| Below the line | Debt Service | Principal and interest on the acquisition loan, if financed |

| Below the line | Net Cash Flow | NOI minus debt service; what the equity holder actually receives each year |

The expense lines are where most first-pass pro formas fall short. A financial model that uses a flat 30 percent expense ratio without itemizing property taxes, insurance, and reserves separately cannot be stress-tested, because a single blended number does not reveal which input is driving the risk. Itemizing each line, the way the calculator above does, is what makes the next step possible.

How to Stress-Test a Pro Forma Before You Rely on It

A pro forma built on a single set of assumptions tells you whether a deal works under one specific version of the future. It does not tell you how much room for error that deal actually has. Stress-testing answers that second question, and it requires changing more than one input at a time.

The three inputs with the most leverage over the outcome are vacancy, exit cap rate, and NOI growth rate. Each interacts with the others, which is why testing them one at a time understates the real risk. A vacancy assumption that moves from 5 percent to 8 percent does more than reduce Year 1 income. It compounds through every subsequent year of the hold, and it changes the Year 1 DSCR result the calculator flags against your minimum threshold.

A practical stress test runs the calculator three times on the same deal: once at base-case assumptions, once with vacancy raised by two to three points and NOI growth cut to zero, and once with the exit cap rate widened by 50 to 75 basis points on top of those same operating assumptions. If the deal still clears its required return and the DSCR pill still reads pass in that third pass, the deal has real margin. If IRR drops below the hurdle or DSCR fails in the moderate scenario, the base case was carrying the deal, not the underlying fundamentals.

This is also the fastest way to catch an aggressive sponsor pro forma. A projection that only works under base-case assumptions, with no disclosed downside scenario, is not evidence the deal is strong. It is evidence the stress test has not been run yet.

Frequently Asked Questions

What is the difference between a pro forma and actual operating statements?

A pro forma is a forward-looking projection built on assumptions you control: rent growth, vacancy, expense inflation. Actuals, typically shown as a trailing twelve months (T12) statement, report what the property has already produced. The gap between the seller's T12 and your pro forma represents the value you are underwriting to create, whether through rent increases, expense reduction, or improved management. A pro forma that simply restates the T12 with no adjustments is not an underwriting exercise. It is a copy of the past.

How often should a pro forma be updated after closing?

Most operators rebuild the pro forma quarterly against actual performance during the first 12 to 18 months of ownership, then shift to an annual budget cycle once the asset stabilizes. The purpose of the early rebuild cadence is to catch divergence from the underwriting assumptions while there is still time to adjust the business plan, rather than discovering the gap at refinance or sale.

What vacancy assumption is reasonable for a stabilized multifamily property?

Five to seven percent is a common base-case range for stabilized market-rate multifamily in most markets, though the right number depends heavily on submarket supply conditions and the property's specific lease expiration schedule. A vacancy assumption below five percent on anything other than a property with long-term, in-place leases is the single most common red flag in a sponsor's pro forma, because it leaves almost no room for normal tenant turnover.

Can a pro forma replace a lender's or LP's third-party underwriting requirements?

No. A self-built pro forma, including the output of this calculator, is appropriate for screening and internal decision-making, but most construction and acquisition lenders, along with institutional LPs, require an independently prepared analysis as a condition of financing or capital commitment. The structural conflict is straightforward: the sponsor benefits if the deal proceeds, so a sponsor-built pro forma cannot serve as its own independent verification.

Why does the calculator separate unlevered and levered IRR?

Unlevered IRR shows the return the asset itself generates, independent of how it is financed. Levered IRR shows the return on the equity actually invested, after debt service. The gap between the two reveals how much of the projected return depends on leverage rather than the property's fundamental performance. A deal with a strong levered IRR but a weak unlevered IRR is a leveraged bet on financing terms holding steady, not a fundamentally strong asset.

What happens if the pro forma and the actual performance diverge significantly after acquisition?

Divergence in either direction should trigger a re-underwriting of the remaining hold period, not just a note for the next investor update. If actual NOI is running meaningfully below the pro forma, the original exit assumptions, refinance timing, and even the hold period itself may no longer be supportable, and continuing to report against the original projection without adjustment understates the real risk to remaining capital. The same discipline applies in reverse: outperformance can justify accelerating a refinance or exit ahead of the original plan.

Share on:

Our Services

Request a Consultation

Schedule a consultation to discuss your next development, acquisition, or market analysis needs

Recent Posts

How to Value Commercial Real Estate: The 3 Approaches Explained

A commercial property can produce three legitimately different appraised values at the same time, and…

NOI in Real Estate: The Number Behind Every Deal, and…

Ask a seller, a buyer, and a lender for the same property net operating income,…

Development Pro Forma: Structure, Mechanics, and Lender Tests

A development pro forma is built backwards from a property that does not yet exist.…