What underwriting means in real estate, why it is the most consequential step in any transaction, and how lenders and investors each approach it differently.

Every real estate deal — the apartment building your neighbor sold, the strip mall down the street, the house you almost bought last year — passed through the same invisible gauntlet before it closed. Money didn’t move until someone sat down with a spreadsheet, a set of assumptions, and a ruthless mandate to answer one question: Does this deal actually work?

That process is called underwriting. It is the engine behind every mortgage approval, every investment decision, and every pass on a deal that didn’t pencil. Understanding it won’t just make you a more informed borrower or investor — it will fundamentally change how you read any real estate opportunity.

What Underwriting Actually Means

Real estate underwriting is the systematic process of analyzing a property and a transaction to determine whether the risk is acceptable and the numbers are sound. The word itself comes from the practice of insurers literally signing their names under a risk they were willing to assume — and that original meaning holds. To underwrite a deal is to stake your judgment (and someone’s capital) on its viability.

Underwriting is not a single conversation or a gut-check. It is a structured, document-heavy, assumption-driven process that scrutinizes the property, the borrower or investor, the market, and the deal structure before capital is committed.

Underwriting is where enthusiasm meets arithmetic. A deal that sounds great at dinner has to survive the spreadsheet at 9 a.m. — and most of the real estate industry runs on that gap.

Two Kinds of Underwriting — Same Deal, Different Lenses

Real estate underwriting is performed by two distinct parties with different objectives. Both are analyzing the same deal — but they are asking fundamentally different questions about it.

| LENDER UNDERWRITING Can we get our money back? Lenders underwrite to assess default risk. Their goal is to confirm the loan will be repaid under a range of market conditions — not to maximize return. | INVESTOR UNDERWRITING Is the return worth the risk? Investors underwrite to assess opportunity. Their goal is to model what the deal will return — and whether that return justifies the capital and risk involved. |

| Primary concern: Debt repayment | Primary concern: Risk-adjusted return |

| Key metric: DSCR, LTV, LTC | Key metric: IRR, equity multiple, cash yield |

| Views property as: Collateral | Views property as: Income-producing asset |

| Scrutinizes: Borrower credit, liquidity, track record | Scrutinizes: NOI, exit assumptions, market |

| Worst-case focus: Will income cover the debt? | Worst-case focus: What’s the downside scenario? |

| Outcome: Approve, condition, or decline | Outcome: Invest, pass, or renegotiate |

The Metrics That Drive Every Underwriting Decision

Underwriting speaks in ratios and returns. These six metrics appear in almost every real estate underwriting model — residential or commercial, lender or investor.

| Abbreviation | Full Term | What It Means | Formula |

|---|---|---|---|

| DSCR | Debt Service Coverage Ratio | How many times over does the property’s income cover its loan payments? A DSCR below 1.0 means the property can’t pay its own debt. | NOI ÷ Annual Debt Service |

| LTV | Loan-to-Value Ratio | What percentage of the property’s appraised value does the loan represent? Higher LTV = less equity cushion = more lender risk. | Loan Amount ÷ Property Value |

| IRR | Internal Rate of Return | The annualized return on invested equity over the full hold period, accounting for all cash flows and the eventual sale proceeds. | Discount rate where NPV = 0 |

| EM | Equity Multiple | Total cash returned to investors divided by total equity invested. A 2.0x EM means you doubled your money before accounting for time. | Total Distributions ÷ Equity In |

| LTC | Loan-to-Cost Ratio | Used in construction and value-add deals. What percentage of the total project cost is being financed? Common in development underwriting. | Loan Amount ÷ Total Project Cost |

| CoC | Cash-on-Cash Return | Annual pre-tax cash flow as a percentage of equity invested. The simplest measure of what a leveraged property pays you each year. | Annual Cash Flow ÷ Equity Invested |

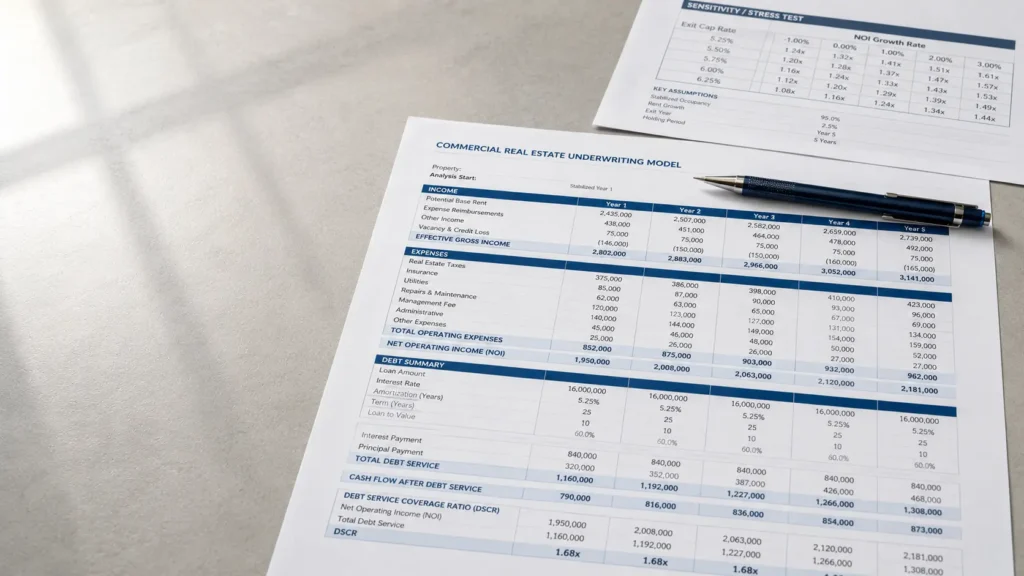

Inside a Real Underwriting Model

Let’s walk through a simplified commercial underwriting model for a 24-unit apartment building — the kind of analysis an investor or lender would actually run before committing capital.

| Line Item | Annual ($) | Notes |

|---|---|---|

| Income | ||

| Gross potential rent | $432,000 | 24 units × $1,500/mo × 12 |

| Vacancy & credit loss (5%) | − $21,600 | Conservative market assumption |

| Other income (laundry, fees) | + $8,400 | Verified from rent rolls |

| Effective Gross Income (EGI) | $418,800 | |

| Operating Expenses | ||

| Property taxes | $42,000 | Per county records |

| Insurance | $18,000 | Quoted from carrier |

| Property management (8%) | $33,504 | 8% of EGI |

| Maintenance & repairs | $24,000 | $1,000/unit/yr |

| Utilities (common area) | $9,600 | Verified from bills |

| Reserves (capex) | $12,000 | $500/unit/yr |

| Total Operating Expenses | $139,104 | 33% expense ratio |

| Returns & Coverage | ||

| Net Operating Income (NOI) | $279,696 | EGI − Expenses |

| Purchase price / value | $3,996,000 | At 7.0% cap rate |

| Loan amount (70% LTV) | $2,797,200 | Lender provides 70% |

| Annual debt service | $189,600 | 6.5% rate, 30-yr am. |

| DSCR | 1.48x | Above 1.25x lender minimum |

| Cash-on-Cash Return | 7.5% | On $1.2M equity invested |

A DSCR of 1.48x tells the lender that for every dollar of debt service due, the property generates $1.48 in income — a comfortable cushion. Most lenders require a minimum of 1.20x to 1.25x. Anything below that threshold triggers a decline or a restructured loan request.

Stress Testing: Where Good Underwriters Earn Their Pay

Any underwriter can make a deal look good under favorable assumptions. The discipline is in stress-testing: what happens if conditions deteriorate? A well-underwritten deal survives adversity. A poorly underwritten one falls apart the moment the market hiccups.

| Scenario | Assumptions | Outcome |

|---|---|---|

| BASE CASE | 5% vacancy, rents flat | As underwritten. NOI of $279,696. DSCR 1.48x. Positive cash flow from day one. |

| DOWNSIDE CASE | 12% vacancy, rents down 8% | NOI falls to approximately $224,000. DSCR compresses to 1.18x, below most lender minimums. The deal still cash flows, but the borrower is operating with very limited margin for error. |

| BEAR CASE | 20% vacancy, rents down 15% | NOI drops to approximately $178,000. DSCR falls to 0.94x, meaning debt service is no longer fully covered. The property becomes a cash drain on the investor. |

Stress testing isn’t pessimism for its own sake. It’s the underwriter’s way of defining the breaking point — and determining whether the investor has enough reserves, equity cushion, and deal structure to survive getting there.

The most dangerous words in real estate underwriting are ‘it’ll work out.’ A deal that only pencils under the best-case scenario isn’t underwritten — it’s hoped for.

Residential Underwriting: The Borrower Is the Asset

In residential real estate, underwriting follows the same logic, but the lens shifts from the property to the borrower. When a homebuyer applies for a mortgage, the lender is underwriting both the collateral (the home) and the person borrowing the money.

Residential mortgage underwriters evaluate four primary factors, sometimes called the Four Cs:

- Capacity — Can the borrower afford the payment? Underwriters calculate debt-to-income ratio (DTI), typically requiring it to stay below 43–45% for conventional loans. Income must be documented, stable, and verifiable.

- Credit — How has the borrower historically managed debt? Credit score, payment history, outstanding balances, and derogatory marks all factor in. Most conventional loans require a minimum 620 score; jumbo and prime loans often require 700+.

- Capital — What reserves and down payment does the borrower bring? More equity means less lender risk. A 20% down payment eliminates PMI; a larger cushion often unlocks better rates.

- Collateral — Is the property worth what the borrower is paying? The appraisal anchors this. If the home appraises below the purchase price, the deal either renegotiates or the buyer brings the gap in cash.

Who Underwrites, and When

| 01 Mortgage lenders & banks Underwrite every residential and commercial loan before approval. This is non-negotiable — no underwriting, no loan. The process takes days to weeks and produces a conditional approval, a full approval, or a denial. | 02 Private equity & institutional investors Run full investment-grade underwriting models on every acquisition. At large funds, a deal may be underwritten by a team of analysts before being presented to an investment committee for a go/no-go decision. |

| 03 Individual real estate investors Anyone buying a rental property, flipping a house, or investing in a syndication should underwrite their own deals — even a simplified model. The math doesn’t care whether you’re a professional. The consequences don’t either. | 04 Syndicators & deal sponsors Operators who raise investor capital underwrite deals to present to limited partners. The sponsor’s underwriting model is the foundation of every investor pitch deck — and the source of most investor due diligence questions. |

Red Flags That Kill Deals in Underwriting

Experienced underwriters develop an instinct for the signals that suggest a deal is being dressed up rather than honestly presented. These are the patterns that most reliably send a deal back for revision — or kill it entirely.

- Pro forma rents with no market support. Projecting rents 20% above current market to make the NOI work is one of the oldest tricks in the book. Underwriters verify against actual comparable leases, not optimistic broker guidance.

- Missing or understated expenses. Property management fees, capital reserves, and vacancy allowances are frequently omitted from seller-provided financials. A real underwrite adds them back, and suddenly the NOI looks very different.

- Compressed exit cap rates. Assuming you’ll sell at a lower cap rate than you bought, without market justification, is wishful thinking built into a financial model. It inflates projected sale prices and IRRs without changing any of the actual deal fundamentals.

- Short interest-only periods masking debt service pressure. Many deals look great while in an IO period. The underwriter must account for the full amortizing payment.

- Borrower liquidity that exists only on paper. A borrower who lists a retirement account as liquid reserves, when withdrawal triggers penalties, isn’t as liquid as stated. Lenders look carefully at the source and accessibility of all claimed assets.

Why Understanding Underwriting Changes Everything

Whether you’re a homebuyer trying to navigate a mortgage approval, an investor evaluating a syndication pitch, or a business owner considering a purchase instead of a lease, underwriting is the framework that separates informed decisions from expensive guesses.

When you understand what an underwriter is looking for, you can prepare a loan application that sails through instead of stalling in conditions. When you understand how an investor underwrites a deal, you can evaluate a sponsor’s projections instead of simply trusting them. When you know what stress tests reveal, you can ask the questions that protect you when markets don’t behave as expected.

Every topic in this series — cap rates, NNN leases, CMAs — feeds directly into the underwriting process. Cap rates determine value and NOI. Lease structures determine income stability. Comparable market data anchors assumptions. Underwriting is where all of those inputs converge into a single verdict: this deal works, or it doesn’t.

Ready to Underwrite Your Next Deal?

Bring us the numbers. We’ll tell you if they hold.

“Underwriting is not the enemy of a good deal — it’s the proof of one. If a deal can’t survive the scrutiny, it was never as good as it looked.”