Ask three people involved in the same deal for the property’s NOI (net operating income), and the answer will likely differ three times.

Net operating income is a property’s revenue minus its operating expenses, calculated before debt service, capital expenditures, depreciation, and income taxes.

In practice, no single NOI exists for a given property. A seller’s in-place NOI, a sponsor’s pro forma NOI, and a lender’s underwritten NOI are typically three different numbers. Reconciling the gaps between them is the core skill of commercial real estate underwriting. This article covers both halves of that skill: how to calculate NOI cleanly, and how to tell when someone else’s NOI number cannot be trusted.

What Is Net Operating Income (NOI)?

NOI in Real Estate measures how much income a property generates from operations alone, stripped of financing decisions, tax position, and accounting treatment. It answers one question: does the real estate itself perform, independent of how it is owned or financed? Lenders, buyers, appraisers, and sellers all start from this number before layering on their own assumptions about debt, taxes, and capital plans.

NOI also converts directly into property value. A buyer’s offer, a lender’s loan size, and an appraiser’s valuation all run through NOI divided by a capitalization rate. Get the NOI wrong by 5%, and the resulting valuation moves by roughly the same percentage. That sensitivity is exactly why NOI gets contested on nearly every deal.

The NOI Formula

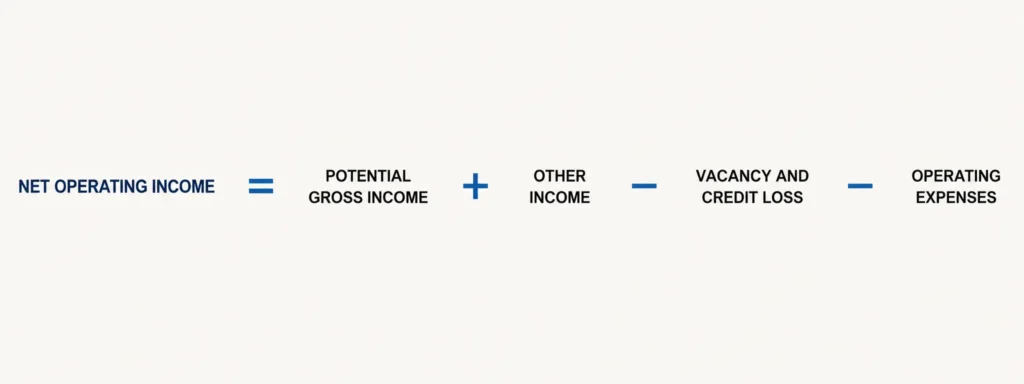

NOI equals effective gross income minus operating expenses.

Effective gross income (EGI) is potential gross income, adjusted for vacancy and credit loss, plus other income. Written as a sequence: potential gross income, less vacancy and credit loss, plus other income, equals effective gross income.

Effective gross income, less operating expenses, equals NOI. Every term in that sequence is calculated before any reference to debt service, capital expenditures, depreciation, or income taxes, the detail most often glossed over in informal explanations.

How to Calculate NOI in Real Estate, Step by Step

Calculating NOI follows the same sequence on every commercial property, regardless of asset class. The inputs change. The structure does not.

Potential Gross Income (PGI)

Potential gross income is the maximum rental revenue a property could generate if every unit or space were leased at market rates with zero vacancy. For multifamily, this is the sum of all unit rents at full occupancy. For office, retail, or industrial space, it is total leasable square footage multiplied by the market lease rate. PGI is a theoretical ceiling, not a forecast: a starting point before any real-world adjustment is applied.

Effective Gross Income (EGI): Vacancy, Credit Loss, and Other Income

Effective gross income brings PGI down to a realistic figure through two adjustments:

- Vacancy and credit loss accounts for unleased units and tenants who fail to pay. Most underwriters apply a vacancy factor between 5% and 10%, depending on market and property type, regardless of a property’s current occupancy. A building that is 100% leased today still gets a vacancy deduction in the pro forma, because turnover and bad debt are a near certainty over any holding period.

- Other income adds back ancillary revenue: parking fees, laundry, storage, pet rent, application fees, and similar line items. On a multifamily property of meaningful scale, other income can run into the tens of thousands of dollars annually and should not be rounded to zero in either direction.

According to underwriting commentary published by Matthews in April 2026, buyers in 2025 underwrote vacancy and credit loss closer to 5%, up from roughly 3% in prior cycles. The shift reflects tighter scrutiny of collections even on stabilized assets.

Operating Expenses

Operating expenses are the recurring costs required to run the property. They typically include:

- Property taxes

- Insurance

- Management fees

- Repairs and maintenance

- Utilities

- Administrative costs

These figures have moved materially in recent underwriting. The same Matthews commentary reports insurance per unit roughly doubling, from about $600 to $1,200 to $1,500. Utilities have climbed from roughly $800 to $900 per unit to around $1,200, and management fees are now underwritten closer to 5% of revenue rather than 3%. An operating expense line not updated to current cost levels will understate true expenses and overstate NOI.

Worked Example: A 50-Unit Multifamily Property

The table below walks a 50-unit multifamily property from potential gross income to NOI, using current underwriting norms for vacancy, other income, and expense ratios.

| Line Item | Annual Amount |

| Potential Gross Income (50 units x $1,800/month average) | $1,080,000 |

| Less: Vacancy and Credit Loss (5%) | ($54,000) |

| Plus: Other Income (parking, pet rent, fees) | $42,000 |

| Effective Gross Income | $1,068,000 |

| Less: Operating Expenses (property tax, insurance, management, repairs, utilities) | ($438,000) |

| Net Operating Income | $630,000 |

At a 5.5% cap rate, that $630,000 NOI supports a valuation of roughly $11.5 million. Move the vacancy assumption from 5% to 8%, a three-point shift a casual review might not flag, and NOI drops to roughly $597,600. At the same cap rate, that single assumption shift removes nearly $590,000 of implied value. This is the mechanical reason pro forma assumptions get scrutinized line by line rather than accepted on the strength of a polished memorandum.

What NOI Excludes (and Why That Matters)

NOI in Real Estate excludes four items, and conflating any of them with an operating expense is the most common error in an informal NOI calculation.

- Debt service, meaning mortgage principal and interest payments, is a financing decision, not an operating cost. The same property generates the same NOI whether it is financed at 50% leverage or owned free and clear.

- Capital expenditures, such as a roof replacement or major HVAC system, are non-recurring investments in the physical asset rather than the cost of operating it day to day.

- Depreciation is a tax and accounting concept with no cash impact in the period it is recognized.

- Income taxes depend on ownership structure and entity-level decisions that have nothing to do with how the property itself performs.

Including debt service inside operating expenses deflates NOI artificially and breaks the purpose of the metric: isolating operating performance from capital structure. Keeping all four exclusions out of the calculation is what allows NOI to be compared meaningfully across properties with different financing, ownership, and tax situations.

How NOI Drives Property Value

NOI in Real Estate converts into value through the capitalization rate, or cap rate: property value equals NOI divided by the cap rate. A property generating $630,000 in NOI at a 5.5% cap rate is worth approximately $11.5 million. At a 6% cap rate, the same NOI supports a value of $10.5 million. Because the cap rate sits in the denominator, even small movements in either figure produce large swings in implied value. That is why both attract intense scrutiny in any transaction above a modest size.

NOI and the Cap Rate

The relationship runs in both directions. A buyer estimating value works forward from NOI and a market cap rate. An appraiser working backward from a known sale price solves for the implied cap rate using the same formula.

Cap rates also compress and expand independently of any single property’s performance, driven by interest rates, capital availability, and investor sentiment. Two identical NOI figures can support sharply different valuations depending on when the cap rate is observed.

A full treatment of cap rate compression and expansion sits outside the scope of this article. The mechanical link to NOI is why any NOI error compounds directly into a valuation error.

How Lenders Use NOI: DSCR and Debt Yield

Lenders run NOI in Real Estate through two underwriting tests before sizing a loan. Debt service coverage ratio (DSCR) divides NOI by annual debt service. According to CBRE’s Q1 2026 lending data, the average DSCR on closed commercial loans stood at 1.36.

Most lenders require a minimum in the 1.20x to 1.25x range. Debt yield divides NOI by the total loan amount. CBRE reported debt yield holding at 9.5% in Q1 2026, consistent with the 9% to 10% range most non-agency lenders target.

Both tests start from the lender’s own NOI figure, not the borrower’s. A lender that disagrees with the borrower’s vacancy, expense, or other income assumptions rebuilds NOI independently before applying either ratio. A borrower’s pro forma NOI and a lender’s underwritten NOI can diverge well before a term sheet is issued.

There Is No Single NOI on Any Deal

Everything covered to this point assumes one clean NOI calculation. In an actual transaction, that assumption breaks down immediately, because a single property generates multiple legitimate NOI figures at the same time depending on who is calculating it and why. Understanding this is the dividing line between a textbook NOI exercise and the way NOI functions on a live deal.

In-Place NOI (the T-12) vs. Pro Forma NOI

In-place NOI, often called the trailing twelve months or T-12, reflects what the property has actually produced over the past year using real rent rolls and expense statements. Pro forma NOI is a forward-looking projection that applies assumptions: market rent growth, a stabilized vacancy rate, updated expense ratios, and sometimes the impact of planned capital improvements. The T-12 is a historical fact. Pro forma NOI is a forecast built on judgment calls, and every judgment call is a place where two parties can reasonably disagree.

The gap between the two numbers is not automatically a red flag. A property that is under-managed or under-rented relative to its market can have a pro forma NOI well above its T-12. That gap can be the entire investment thesis behind a value-add acquisition. The relevant question is never whether a gap exists, but whether it is explained, line by line, with assumptions a third party can independently verify.

Seller’s NOI, Buyer’s NOI, and Lender’s NOI

Beyond the T-12 versus pro forma distinction, the same property typically carries at least three more NOI variants once a transaction is underway, summarized below.

| NOI Variant | Who Calculates It | Where Assumptions Typically Diverge |

| Seller’s NOI | Seller or listing broker, presented in the offering package | Vacancy understated, management fee below market, ancillary income annualized optimistically |

| Buyer’s NOI | Buyer’s underwriting team, used to set the offer price | Vacancy and expenses conservatively adjusted, reserves added, often before due diligence is complete |

| Lender’s NOI | Lender’s credit team, used to size the loan via DSCR and debt yield | Built independently of either party’s number, frequently the most conservative of the three |

| Pro Forma (Year 1) NOI | Sponsor, used in the offering memorandum to project returns to investors | Forward-looking growth and stabilization assumptions layered on top of the T-12 |

No party in this table is necessarily acting in bad faith. A seller has every incentive to present the most favorable defensible number, and a lender has every incentive to present the most conservative one. The skill separating an experienced underwriter from a casual reviewer is knowing exactly where each party’s number is likely to diverge, and why.

Where Sponsors Inflate Pro Forma NOI

The gap between a sponsor’s pro forma NOI and a defensible number tends to concentrate in five specific places. Naming them precisely is more useful than a general warning that projections can be optimistic.

The Vacancy Assumption

Vacancy is the single most common point of inflation. A sponsor presenting a 3% vacancy and credit loss assumption in a market where comparable assets run 5% to 8% is building on a number the asset has not demonstrated. Even a fully leased property in-place still warrants a vacancy deduction, since turnover and bad debt occur over any realistic holding period.

A vacancy assumption that sits meaningfully below the submarket’s trailing average is the first place to apply pressure. The exception is when the sponsor documents a specific reason tied to the asset’s own leasing history.

Management Fees and Reserves

Management fees quoted below market rate for a property of that scale lower reported operating expenses and inflate NOI without changing anything about how the property is actually run. Underwriting data from Matthews shows management fees moving toward 5% of revenue, up from roughly 3% in prior years. A pro forma still running a 3% management fee assumption in 2026 is either working from stale data or deliberately understating expenses.

Reserves for replacement are funds set aside for future capital items like roofs and HVAC systems. They are sometimes omitted from a pro forma entirely or set at a token level. Lenders typically add these back at $250 to $500 per unit annually for multifamily assets if the sponsor has not already included them. An omitted reserve line does not avoid the cost. It only delays who notices it.

Other Income and Expense Ratio Gaps

Ancillary income, parking, laundry, pet rent, and similar fees, gets overstated when a sponsor grosses up these figures to a hypothetical 100% occupancy. The property’s actual occupancy history should set the baseline instead. A pro forma showing other income growing faster than the unit count or the comparable market would suggest deserves a direct question about the basis for that growth.

Expense ratio gaps appear when a sponsor’s total operating expense line sits noticeably below the ratio observed on comparable assets in the submarket. Expense ratio is expressed as a percentage of effective gross income. A pro forma assuming 2018-era insurance and utility costs in a 2026 underwriting model is not aggressive. It is outdated, and outdated assumptions inflate NOI just as effectively as deliberately optimistic ones.

How to Stress-Test a Pro Forma NOI

Identifying where inflation tends to occur is the first half of the discipline. Confirming whether it has occurred on a specific deal requires a repeatable process, not a general sense of skepticism.

Reconciling the T-12 to Year 1

Every dollar of difference between the T-12 and the sponsor’s projected Year 1 NOI should be attributable to a specific, named adjustment. That might be a vacancy assumption that differs from trailing performance, a rent growth assumption on in-place leases, an expense line updated or removed, or a new management contract.

If the sponsor’s materials present the T-12 and the pro forma side by side without a line-item bridge connecting the two, that absence is itself informative. A defensible pro forma can always show its work. One that cannot is asking the reviewer to accept the gap on faith.

Rebuilding the Number Independently

The most reliable stress test is rebuilding NOI from source documents rather than reviewing the sponsor’s summary. That means requesting the actual rent roll, not a unit count and an average rent figure, along with the trailing twelve months of operating statements. It also means requesting the specific vacancy, expense, and other income assumptions used to bridge from the T-12 to the pro forma.

Comparable rent and expense data for similar assets in the submarket provides the external check against the sponsor’s internal logic.

A buyer, lender, or limited partner who rebuilds NOI from these sources will know within a single pass whether the projected number reflects the asset. The alternative is that it reflects an outcome the sponsor wanted to reach. This is, in practice, the same exercise a lender’s credit team runs before issuing a term sheet, applied a step earlier in the process.

How BlueStar Consulting Approaches NOI Underwriting

BlueStar Consulting builds and reviews pro forma NOI as part of its investment analysis, underwriting and due diligence work. The team reconciles sponsor projections against trailing performance, comparable market data, and lender-grade assumptions before capital moves. Investors and developers working through an acquisition, refinance, or LP review can engage Bluestar for an assessment that pinpoints where a projected NOI diverges from a defensible one.

NOI in Real Estate Frequently Asked Questions

What is the difference between NOI and cash flow?

NOI in Real Estate measures a property’s operating performance before any financing is applied. Cash flow, often called cash flow before taxes, takes NOI and subtracts debt service, since most owners hold property with a mortgage in place. Two properties can have identical NOI and meaningfully different cash flow if they carry different amounts of debt. NOI isolates the asset’s performance, while cash flow reflects what an owner actually receives after meeting loan obligations.

Is NOI in Real Estate calculated before or after taxes?

NOI in Real Estate is calculated before income taxes. Taxes depend on the ownership entity, depreciation schedule, and other factors specific to the owner rather than the property. They are excluded to keep NOI a clean measure of operating performance, comparable across different ownership structures.

What is a good NOI for a commercial property?

There is no universal dollar figure that qualifies as a good NOI, since the right number depends on the property’s size, asset class, and market. The more useful benchmark is NOI relative to value and debt service. A property whose NOI supports a DSCR above 1.25x and a debt yield above roughly 9% to 10% clears standard underwriting thresholds for that loan size.

What is the difference between in-place NOI and pro forma NOI?

In-place NOI, also called the T-12, reflects what a property has actually earned over the trailing twelve months based on real rent rolls and expense statements. Pro forma NOI is a forward-looking projection built on assumptions about rent growth, stabilized vacancy, and updated expenses. The T-12 is historical fact. Pro forma NOI is a forecast, and the gap between the two should always be explainable through specific, named assumptions rather than accepted at face value.

How much can a sponsor’s pro forma NOI legally or reasonably differ from the T-12?

There is no fixed percentage that defines a reasonable gap, since a legitimate value-add thesis can justify a substantial difference between trailing and projected NOI. What matters is whether every dollar of that gap ties to a specific, verifiable assumption. That might be a documented rent growth rate, a vacancy adjustment grounded in submarket data, or a planned operational change. A gap with a clear line-item bridge is a business plan. A gap without one is a number that has not yet been tested.