Most real estate investment analyses tell you whether a deal looks good. The ones that actually protect capital tell you something different: which assumptions have to hold for the deal to work, and what happens to returns when one of those assumptions breaks. That distinction separates institutional-grade analysis from a spreadsheet built to confirm a decision already made.

Real estate investment analysis is the structured evaluation of a property’s financial performance, risk profile, and return potential. It applies metrics, including net operating income (NOI), internal rate of return (IRR), equity multiple, and debt service coverage ratio (DSCR) to determine whether an acquisition or development meets the return threshold required for a go decision. A rigorous analysis goes further than a single projected return: it models multiple scenarios, tests key assumptions against market data, and identifies the conditions under which the deal fails to reach its target.

The Metrics That Drive the Decision

Every real estate analysis uses a standard set of metrics. What separates institutional underwriting from basic due diligence is not which metrics are included. It is whether the analyst understands what each metric cannot tell you.

| Metric | What It Measures | Primary Limitation |

| Net Operating Income (NOI) | Annual income from operations after expenses, before debt service | Ignores capital expenditure timing and lease-up risk; a single snapshot |

| Capitalization Rate | NOI divided by asset value; an unlevered yield on current operations | Backward-looking; does not reflect rent trajectory, vacancy risk, or capital needs |

| IRR (Internal Rate of Return) | Annualized return on equity over the full hold period, accounting for time value of money | Dependent entirely on exit assumptions; can be engineered by adjusting hold period or exit cap rate |

| Cash-on-Cash Return | Annual cash flow after debt service divided by equity invested | Ignores total return and exit value; tells the current yield story only |

| Equity Multiple | Total distributions divided by total equity invested | Ignores timing; 2.0x in three years and 2.0x in ten years produce the same multiple |

| DSCR (Debt Service Coverage Ratio) | NOI divided by annual debt service | A lender’s metric; does not capture the equity investor’s risk exposure or return profile |

None of these evaluation metrics functions well in isolation. IRR without an equity multiple misses the total return story. DSCR without NOI stress-testing misses the margin of safety. The value of the framework is in how the metrics interact, not in what any single number reports.

What Risk-Adjusted Returns Actually Measure

The term risk-adjusted return appears in most investment analyses but is rarely calculated explicitly. In practice, it requires a comparison: the return the investment generates relative to the risk the investor accepts to earn it.

The simplest version of this comparison is the spread between the unlevered IRR (the project-level return before debt is applied) and the risk-free rate. In mid-2026, the 10-year US Treasury yield sits in the 4.3 to 4.5 percent range. A stabilized core multifamily asset with an unlevered IRR of 5.5 to 6.5 percent is generating a risk premium of 100 to 200 basis points above the risk-free rate. That spread must justify the illiquidity, the operating complexity, and the execution risk the investor is absorbing. For most institutional capital, that spread is insufficient unless the asset has long-term lease structure, strong credit tenants, or other risk-mitigating characteristics.

Value-add and development deals require higher risk premiums for precisely that reason. A deal with an 18 percent levered IRR generating only a 6 percent unlevered return is highly leveraged: the return is being manufactured by the debt, not by the underlying asset. If the exit does not materialize as projected, leverage amplifies the loss as effectively as it amplified the gain.

The practical application is this: a deal with an 11 percent unlevered IRR and a 16 percent levered IRR is a fundamentally stronger deal than one with a 6 percent unlevered IRR and a 20 percent levered IRR, even though the second deal advertises a higher headline return. Risk-adjusted analysis reveals the difference. A headline return projection without the unlevered return calculated alongside it is incomplete.

How to Build a Scenario Analysis That Means Something

The most common failure in scenario analysis is presenting three versions of the same optimistic assumptions with minor adjustments. A downside scenario that reduces rent growth from 4.5 percent to 3.5 percent, while leaving the exit cap rate and vacancy assumptions unchanged, is not a stress test. It is a sensitivity toggle.

A credible scenario analysis forces the analyst to consider how the most critical assumptions interact under adverse conditions. In a value-add acquisition, those assumptions are renovation timeline, rent uplift at stabilization, and exit cap rate. In a development deal, they are construction cost, lease-up velocity, and the capital market environment at exit. The table below applies this framework to a representative acquisition.

$10,000,000 Multifamily Acquisition | 72 Units | Sun Belt Market

Purchase Price: $10,000,000 | Loan: $6,500,000 at 6.75% IO | Total Equity: $4,300,000 (includes $800K renovation)

| Assumption | Downside | Base Case | Upside |

| Vacancy | 9% | 6% | 4% |

| Rent growth per year | Flat (0%) | 3.0% | 4.5% |

| Renovation completion | Month 28 | Month 18 | Month 14 |

| Exit cap rate | 6.25% | 5.50% | 5.00% |

| Stabilized NOI | $545,000 | $650,000 | $715,000 |

| Year 5 NOI | $545,000 | $690,000 | $785,000 |

| Exit value | $8,720,000 | $12,545,000 | $15,700,000 |

| Net equity at exit | $2,089,000 | $5,857,000 | $8,965,000 |

| Levered IRR | -8.3% | 10.4% | 20.3% |

| Equity multiple | 0.58x | 1.58x | 2.38x |

The same acquisition, the same capital structure, and a 28-point range in levered IRR. That range is not a modeling anomaly. It is the actual risk profile of the deal. Every projection that presents only the middle column is withholding the information an investor most needs to make a sound decision.

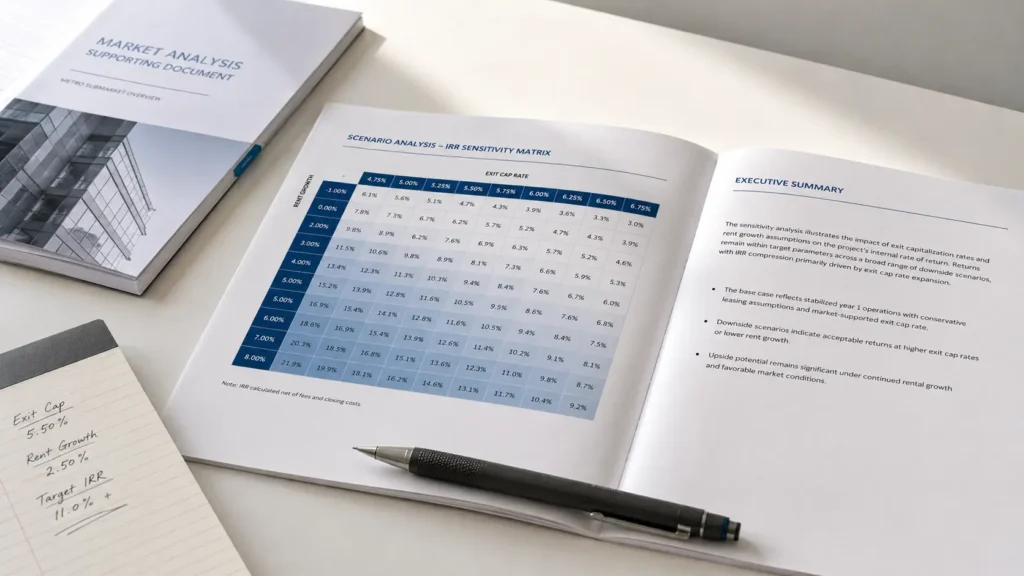

Sensitivity Analysis: The Three Inputs That Actually Move the Needle

Sensitivity analysis tests how returns change when a single variable shifts while others remain constant. The value of this exercise depends entirely on which variables are tested.

The three inputs with the highest leverage on returns across almost all deal types are the exit cap rate, rent growth at stabilization, and, in development deals, construction cost per square foot.

According to analysis from March Associates’ 2026 construction market report, a $2 to $4 million cost gap between initial underwriting and contractor buyout is common on $40 million ground-up projects, representing a 5 to 10 percent cost overrun that compresses returns directly. A 50 basis point expansion in the exit cap rate on a $10 million NOI property reduces the projected sale price by $1.7 to $2 million. A 5 percent downward revision to projected rent growth over a five-year hold compresses levered IRR by 150 to 300 basis points, depending on the leverage ratio.

The inputs that move the needle least and are most frequently used to make a model look stronger are expense ratios beyond Year 1, vacancy in the out-years of the hold, and general and administrative cost growth. A sensitivity table that tests only rent growth while holding the exit cap rate fixed provides one dimension of a two-dimensional problem. The most useful format tests the two highest-leverage variables simultaneously, in a matrix that shows returns across all combinations. That matrix is what an investment committee will run independently if the sponsor does not provide it first.

What Kills a Deal at the Investment Committee Level

Investment committees do not reject deals because the projected returns are too low. They reject deals because the assumptions underlying those returns are not defensible. The distinction matters, because sponsors who understand this distinction build their analysis to pre-empt the committee’s objections rather than respond to them.

The following signals are consistent indicators that a submission will be challenged or declined:

| Red Flag | What the Committee Reads Into It |

| Terminal cap rate assumption below the going-in cap rate | The sponsor is projecting cap rate compression as a return driver, not asset performance |

| Rent growth assumption above the submarket’s trailing 3-year average | The model is pricing in conditions that haven’t materialized yet and may not |

| Expense ratio below 30% on multifamily | A well-documented underwriting error; lenders and appraisers reject it, and it inflates NOI directly |

| Vacancy assumption below 5% in a transitional or value-add asset | Forces the lease-up to work perfectly; a single quarter of delay invalidates the model |

| Sensitivity analysis that tests one variable | Signals that compounding adverse conditions have not been modeled |

| No downside case, or a downside case within 200bps of the base IRR | The sponsor has not seriously stress-tested the deal |

| Single-point IRR with no scenario range | The number presented as “the return” conceals the distribution of possible outcomes |

| Construction costs based on rule-of-thumb per-square-foot without a contractor quote | Cost inputs will not survive the bid process in the current environment |

According to Walker and Dunlop Investment Partners’ May 2026 analysis of current CRE risks, many construction loans made in the first half of the decade have come due under the shadow of properties not hitting the rents they were underwritten at, primarily because deals were stress-tested against a backdrop of cheap capital and high rent growth rather than the conditions that actually materialized. The investment committee’s job is to identify which current-cycle assumptions are subject to the same dynamic.

The Investment Memo: What Gets Deals Funded

The investment memo is the analytical summary that translates the model into a decision. It is distinct from the pitch deck: the deck creates interest, the memo creates conviction, and the committee votes on the memo.

A memo that gets funded covers six elements in a specific order. The executive summary states the investment thesis, the key metrics, and the target return range in under 200 words. The market analysis establishes the submarket’s demand drivers with data sourced to a specific comparable set, not metro-level averages. The financial analysis presents the full model, including unlevered and levered returns, all three scenario cases, and the sensitivity matrix.

The risk section names each material risk explicitly and explains the mitigation; a memo that does not acknowledge risks does not instill confidence, it raises suspicion. The capital structure section details the sources and uses, the debt terms, and the waterfall mechanics for LP and GP distributions. The exit strategy presents the base exit thesis and at least one alternative path: sale, refinance, or hold-for-yield.

The memos that fail at committee share a structural problem: they build toward the return rather than from the asset. A committee reviewing a memo structured around the projected IRR is being asked to accept the conclusion before evaluating the evidence. A memo structured around the asset, the market, and the risks is presenting the evidence first and letting the committee reach its own conclusion. That sequence is the difference between a presentation that creates buy-in and one that generates skepticism.

How Bluestar Consulting Approaches Investment Analysis

BlueStar Consulting builds institutional-grade investment analysis for developers, investors, and project sponsors across acquisition, value-add, and development strategies. Every engagement produces a full three-scenario financial model with sensitivity analysis, unlevered and levered returns presented together, and a clear identification of the assumptions with the most leverage on outcomes.

Sponsors preparing for investment committee review, LP presentation, or lender due diligence can engage Bluestar for model construction, independent analysis, or assumption validation against current submarket data.

Real Estate Investment Analysis Frequently Asked Questions

What is the difference between IRR and risk-adjusted return in real estate?

IRR is a return metric: it measures the annualized rate at which an investor’s capital grows over the hold period. Risk-adjusted return is a performance evaluation framework: it places the IRR in context by comparing it to the risk the investor accepted to earn it. A 15 percent levered IRR on a core stabilized asset and a 15 percent levered IRR on a ground-up development are not equivalent opportunities. The development carries construction risk, entitlement risk, lease-up risk, and a cash-negative carry period. Risk-adjusted analysis quantifies the premium the development must offer over the stabilized asset to justify those additional risks.

Which metrics should an investor prioritize when evaluating a sponsor’s deal?

The most diagnostic combination is unlevered IRR, levered IRR, equity multiple, and DSCR on the stabilized asset. Unlevered IRR reveals whether the asset itself generates returns, independent of the debt structure. The gap between unlevered and levered IRR shows how much of the projected return is leverage-driven. The equity multiple cross-checks whether the IRR reflects genuine capital growth or a short-hold with modest absolute gain. DSCR on the stabilized NOI confirms whether the asset can service its debt under a conservative occupancy assumption.

What is a realistic IRR target for a multifamily value-add deal in 2026?

Levered IRR targets in the 12 to 18 percent range are typical for market-rate multifamily value-add strategies in Sun Belt markets in 2026, based on going-in cap rates in the 5.0 to 5.5 percent range and exit assumptions that do not project cap rate compression. Deals underwriting to 20 percent or above on levered IRR at these entry prices typically carry either high leverage, aggressive rent growth assumptions, or both. A levered IRR in that range warrants scrutiny of the exit cap assumption and the sensitivity to a 50 to 100 basis point expansion.

How should an investor evaluate a scenario analysis provided by a sponsor?

The key test is whether the downside scenario is genuinely adverse or merely a modest haircut to the base case. A credible downside case changes at least two of the three highest-leverage assumptions simultaneously: typically the exit cap rate and the rent growth or vacancy assumption. The resulting IRR in the downside case should fall below the investor’s minimum return threshold, which is the point: the downside case should reveal the conditions under which the deal fails. A downside that still meets the target return is not a stress test. It is a repackaged optimistic scenario.

What distinguishes an investment memo that gets funded from one that does not?

The structural difference is whether the memo presents evidence first or conclusions first. Memos that lead with the projected return and then support it with market data are asking the reader to accept the conclusion before evaluating the evidence. Memos that lead with the asset, the market, and the risk analysis create conviction by the time the return projections appear. Beyond structure, the single most common reason memos fail at committee is an unacknowledged risk: a committee that has to surface a material risk the sponsor did not address will assume the sponsor either missed it or chose not to disclose it. Neither reading is favorable.